Tax compliance can be overwhelming, especially for small businesses, professionals, and freelancers. To simplify tax calculations and reduce the burden of maintaining detailed accounts, the Indian government introduced the Presumptive Taxation Scheme (PTS). But what exactly is presumptive taxation, and how does it work? This article provides a comprehensive guide on presumptive taxation, its eligibility, benefits, and tax implications

Table of Contents

What is Presumptive Taxation?

Presumptive taxation is a simplified method of taxation introduced under the Income Tax Act, 1961, to reduce the compliance burden for small taxpayers. Under this scheme, taxpayers can declare income at a prescribed rate, eliminating the need to maintain extensive financial records and get accounts audited.

This scheme is mainly applicable under Section 44AD, 44ADA, and 44AE of the Income Tax Act, targeting small businesses, professionals, and transporters.

Sections Under Presumptive Taxation Scheme

1. Section 44AD – For Small Businesses

- Applicable to individuals, HUFs, and partnership firms (except LLPs) engaged in any business.

- Turnover should not exceed Rs. 3 crore (as per Budget 2023, with 95% digital transactions; otherwise, Rs. 2 crore).

- Presumptive income is deemed to be 8% of total turnover (or 6% if receipts are digital).

- No need to maintain books of accounts or tax audits.

2. Section 44ADA – For Professionals

- Applicable to specified professionals such as doctors, lawyers, architects, engineers, accountants, and consultants.

- Gross receipts should not exceed Rs. 75 lakh.

- Presumptive income is 50% of total gross receipts.

- No requirement for maintaining books of accounts or tax audit.

3. Section 44AE – For Transporters

- Applicable to taxpayers owning up to 10 goods vehicles.

- Presumptive income is calculated as Rs. 1,000 per ton per month for heavy vehicles and Rs. 7,500 per month per vehicle for others.

- No requirement for keeping detailed financial records.

Benefits of Presumptive Taxation Scheme

The presumptive taxation scheme provides several advantages:

- Ease of Compliance: No need to maintain detailed books of accounts.

- Tax Savings: Lower taxable income due to fixed presumptive rates.

- No Audit Requirement: Small businesses and professionals are exempt from mandatory audits.

- Simplified Return Filing: Taxpayers can file returns with minimal documentation.

- Encourages Digital Transactions: Offers lower tax rates for digital payments.

Limitations of Presumptive Taxation

While presumptive taxation is beneficial, it has certain limitations:

- Not Available for LLPs and Companies: Only individuals, HUFs, and partnership firms (excluding LLPs) can avail of this scheme.

- Fixed Income Calculation: Actual profit/loss is ignored, which may not always be beneficial.

- Opting Out Restrictions: If a taxpayer opts out of the scheme after availing it, they cannot re-enter for the next five years.

- No Deductions Allowed: Expenses such as rent, depreciation, and salaries cannot be separately claimed.

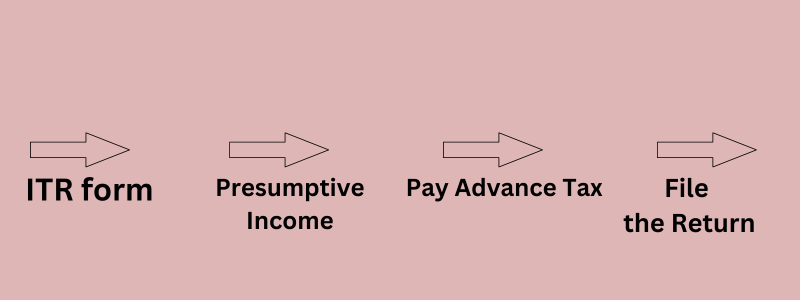

How to File Income Tax Returns Under Presumptive Taxation?

Filing returns under presumptive taxation is straightforward. Follow these steps:

- Choose the Appropriate ITR Form:

- ITR-4 is used for individuals and HUFs opting for presumptive taxation.

- ITR-3 is used if a business/professional does not opt for the scheme.

- Report Presumptive Income:

- Mention total turnover or receipts.

- Declare income at the prescribed rate.

- Pay Advance Tax (if applicable):

- If total tax liability exceeds Rs. 10,000, advance tax must be paid by March 15 of the financial year.

- File the Return on Time:

- The due date for filing ITR under presumptive taxation is July 31 of the assessment year.

Who Should Opt for Presumptive Taxation?

Presumptive taxation is ideal for:

- Small business owners with turnover below Rs. 3 crore.

- Freelancers and professionals with receipts up to Rs. 75 lakh.

- Transporters with a small fleet of vehicles.

- Taxpayers who want to avoid compliance burdens.

Recent Updates and Changes

- The turnover limit under Section 44AD was increased from Rs. 2 crore to Rs. 3 crore (if digital transactions exceed 95%).

- Gross receipts limit under Section 44ADA was increased from Rs. 50 lakh to Rs. 75 lakh.

- More businesses and professionals are opting for presumptive taxation due to ease of filing and compliance.

Conclusion

Presumptive taxation is a beneficial scheme for small businesses and professionals, offering simplicity, reduced compliance, and tax-saving opportunities. If your income falls within the prescribed limits and you prefer hassle-free taxation, opting for presumptive taxation can be a smart decision.

Before choosing this scheme, consult a tax expert to ensure it aligns with your financial goals. If you need more guidance on taxation and financial planning, explore more articles on FinanceSastra.com.

FAQs on Presumptive Taxation

Q1. Is presumptive taxation mandatory? A: No, it is optional. However, once opted in, you must follow the scheme’s rules for five years.

Q2. Can I claim deductions under presumptive taxation? A: No, all business expenses are deemed covered in the presumptive income.

Q3. What happens if my turnover exceeds the limit? A: If turnover exceeds the limit, you must maintain books of accounts and file regular ITRs.

Q4. Can I opt for presumptive taxation if I have multiple businesses? A: Yes, but the total turnover of all businesses should not exceed the prescribed limit.

For more tax-saving tips and financial insights, stay tuned to FinanceSastra!